Digital Asset Trading Infrastructure for Banks: Core Components

Banks face fragmented markets, legacy systems, and regulatory complexity. Learn what digital asset trading infrastructure financial institutions need to operate at scale.

Last updated on Tue May 19 2026

The early phase of the internet was a chaotic playground for enthusiasts, startups, and pioneers pushing technological boundaries. They proved the technology worked but faced many challenges: it was fragmented, lacked essential infrastructure, and failed to gain broad institutional trust.

The internet’s real breakthrough came when large institutions stepped in. They provided scale, reliability, and resilience, transforming the technology into a global infrastructure for secure payments and thriving commerce.

A similar turning point is now emerging in the digital asset space. Early adopters have demonstrated strong demand. To make this market truly global, sustainable, and trustworthy, however, the active engagement of financial institutions is essential.

These institutions face significant hurdles: fragmented digital assets markets, incompatible legacy systems, regulatory requirements, and the inherent complexity of institutional setups. Facing these challenges and adopting digital assets as a big player will make cryptocurrencies, tokenized securities, stablecoins and other asset classes accessible to anyone.

What Digital Asset Trading Infrastructure for Banks Actually Requires

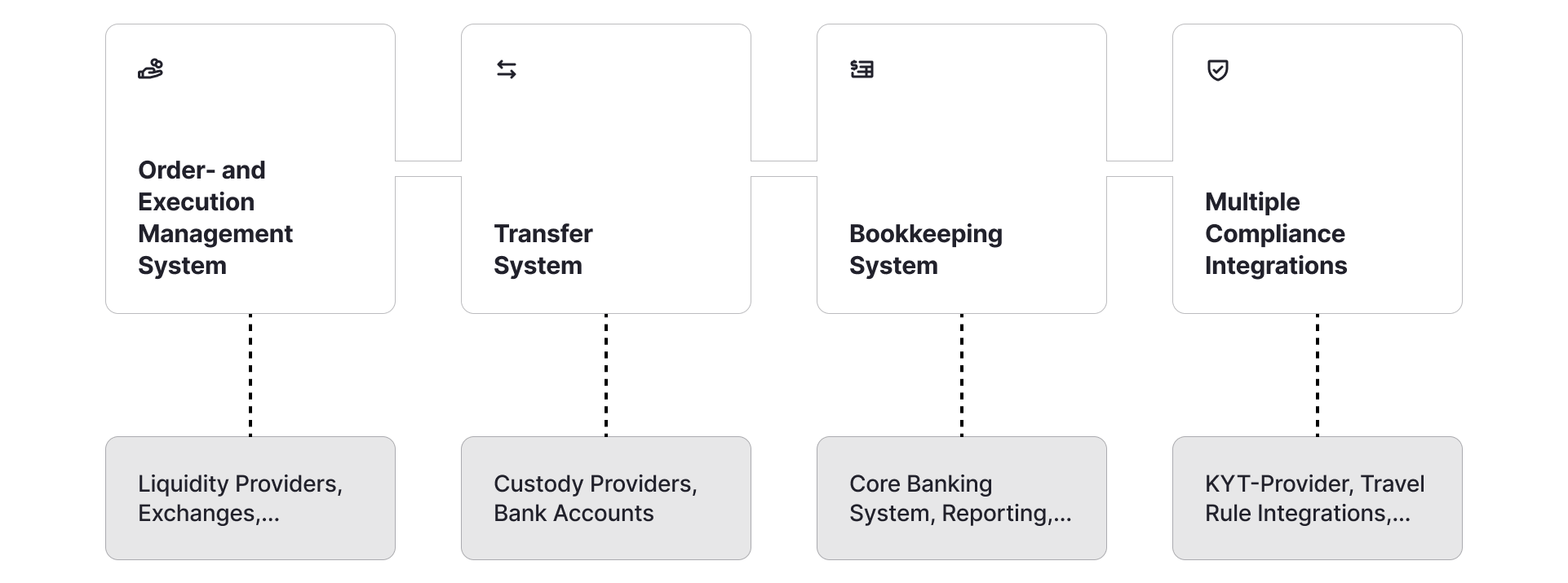

Operating digital assets at institutional scale demands systems built specifically for their characteristics. Traditional infrastructure was not designed for 24/7 markets, assets with 18 decimal places, or on-chain settlement. Four components are non-negotiable:

- Order and Execution Management System (OEMS): Digital markets operate continuously, and trading often occurs in tiny fractions. Banks need an OEMS that keeps pace, ensuring every order is executed smoothly across multiple venues. Traditional systems were not built for these requirements.

- Transfer System: In treasury operations, value must move securely across different networks, at speed, and always in compliance. Only a purpose-built transfer system can initiate, monitor, and automate on-chain transactions. Traditional institutional transfer systems do not support this.

- Bookkeeping System: Every balance, fee, and transaction must be tracked with absolute precision. Clients expect trust in their holdings, and regulators demand complete traceability under MiCAR record-keeping requirements. Reconciliation down to the last decimal is essential.

- Multiple Compliance Integrations: KYT, Travel Rule, and Trade Surveillance are all integral to institutional digital asset operations. Together, they represent a significant layer of complexity that the infrastructure must handle natively.

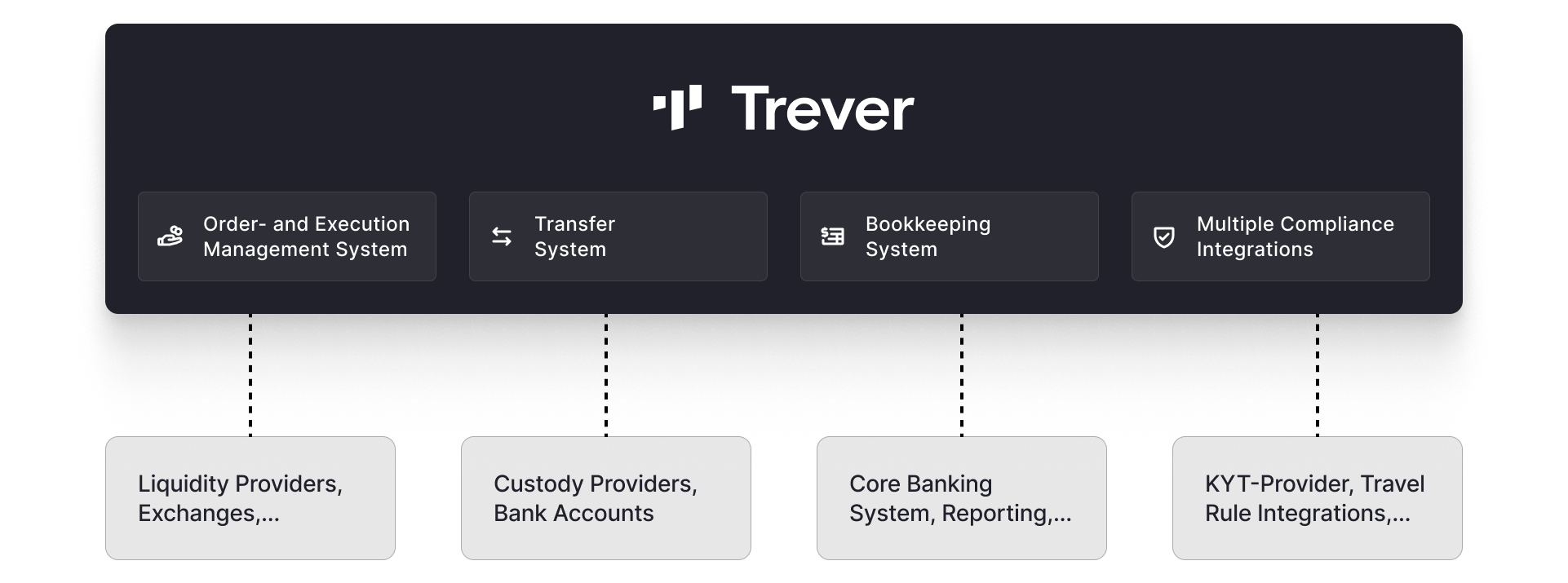

The Foundation: A Single Integrated System

Just as the internet needed servers, browsers, and operating systems to become usable at scale, digital assets need infrastructure that makes them accessible to any institution. We truly believe that in the future, every tradable asset, from securities and bonds to stablecoins and real-world assets, will be on the blockchain. Trever enables banks to interact with these assets operationally.

Trever's Digital Asset Operating System provides this foundation. Instead of a patchwork of tools, a single integrated system manages the entire lifecycle of digital assets:

- Modular: start with core functionality, expand as requirements grow

- Automated: reduce manual work and operational risk

- Interconnected: bridge digital asset workflows with legacy core banking systems

- Scalable: from trading and custody to tokenized securities and beyond

The right digital asset trading infrastructure is what empowers banks to innovate and lead with confidence. For more information, contact our experts at contact@trever.io

Frequently Asked Questions

Why can't banks use their existing core banking infrastructure for digital assets?

Should banks build digital asset trading infrastructure in-house or buy it?

What are the core components of digital asset trading infrastructure for banks?

Disclaimer: The information provided in this blog post is marketing content, reflects the status at the time of publication, is non-binding, and is intended for general informational purposes only. Trever GmbH does not assume responsibility for the completeness, accuracy, timeliness, or suitability of the information for any particular purpose, and readers should not rely on it as the sole basis for any decision.

This content does not constitute legal, regulatory, tax, accounting, investment, financial, or other professional advice, nor does it constitute or should it be interpreted as an offer, solicitation, recommendation, or invitation to buy, sell, subscribe for, exchange, hold, or otherwise transact in any crypto-assets, digital assets, financial instruments, securities, or other assets. Readers should conduct their own assessment before making legal, regulatory, financial, investment, or business decisions.

Trever GmbH provides software and infrastructure solutions for institutional digital asset operations and does not provide investment advice, portfolio management, or any other regulated financial, investment, or crypto-asset services to investors or end customers.

- Check our latest news articles

- Follow us on LinkedIn